Blog

3 Banking Regulation Trends Investors Should Know

Banking regulation rarely makes for thrilling headlines, but seasoned investors know better than to ignore it. The rules governing banks shape how much they can lend, what returns they can deliver, and how the financial system behaves under stress. When regulations change, sectors rise and fall, capital flows reroute, and new asset classes move from the fringe to the mainstream.

Right now, three regulatory trends stand out as especially important for anyone with money in the markets. Here’s what they are and why they matter to your portfolio.

1. Digital Asset Rules Are Maturing

For years, the biggest question hanging over cryptocurrency was regulation. Banks were largely kept at arm’s length from digital assets, exchanges operated in legal gray zones, and institutional investors stayed on the sidelines waiting for clarity. That era is ending.

Governments around the world have moved from debating whether to regulate digital assets to deciding how to do so, with frameworks emerging for stablecoins, custody standards, and exchange oversight. Clearer rules tend to invite bigger players, and the gradual opening of the banking system to digital assets is one of the most consequential shifts in modern finance.

New trading platforms like LeveX offer modern entry points for newcomers and experienced traders as digital assets continue their march into the financial mainstream. As always with an evolving asset class, position sizing and risk management matter as much as platform choice, but the direction of travel is clear. Crypto is becoming part of the regulated financial landscape, not an exception to it.

2. Capital Requirements Keep Tightening for Big Banks

The second trend traces back to the 2008 financial crisis and refuses to fade: regulators keep pushing large banks to hold more capital against their risks.

The latest round, often called the Basel III endgame, would require the largest institutions to bolster their capital buffers further, and banks have pushed back hard, warning that stricter requirements would constrain lending and squeeze returns. The 2023 regional bank failures added fuel, prompting fresh scrutiny of mid-sized banks that had previously enjoyed lighter treatment.

Investors care because capital rules directly affect bank profitability. Higher requirements can mean lower returns on equity, smaller buybacks, and more conservative dividend policies, all central to the investment case for bank stocks. They also shape the competitive landscape, as lending that becomes expensive for banks migrates to private credit funds and other less-regulated players, one reason private credit has exploded into a trillion-dollar asset class.

The gap between a proposal and a final rule is often where the market misprices bank stocks, and investors who understand what’s actually in the rules, rather than the lobbying headlines, get a real analytical edge.

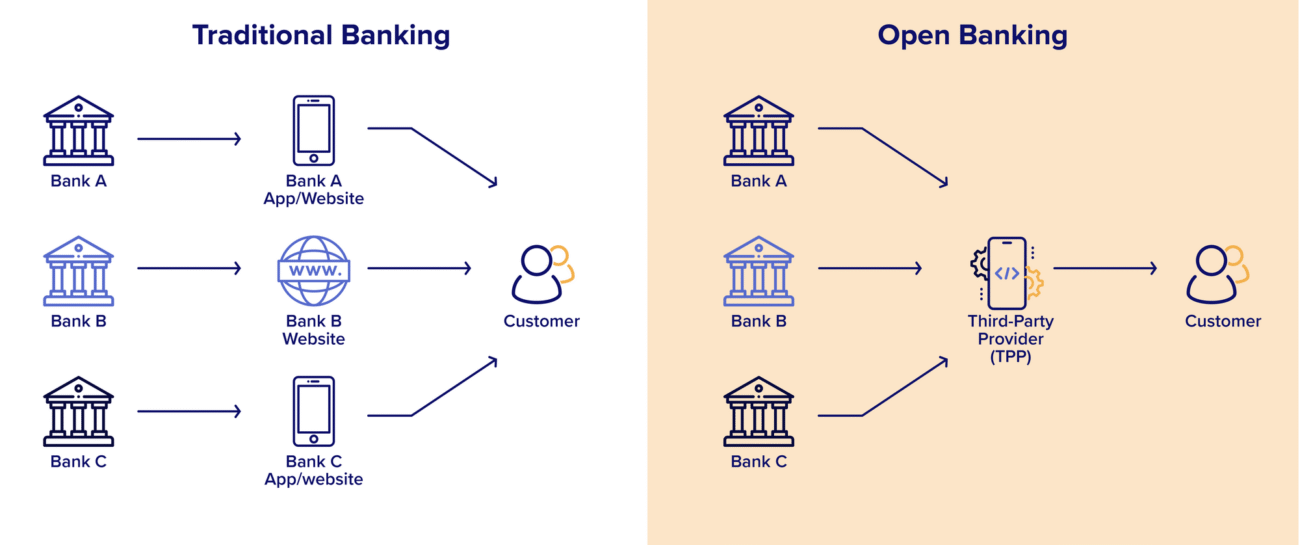

3. Open Banking Is Rewiring Who Owns the Customer

The third trend is quieter but may prove the most transformative: open banking. Regulators in the United States have finalized rules requiring banks to allow customers to securely share their financial data with third parties free of charge. In plain terms, your checking account history no longer belongs exclusively to your bank. It belongs to you, and you can hand it to any app or service you choose.

That sounds technical, but the investment implications are sweeping. Open banking lowers the moat incumbent banks have enjoyed for generations, in which switching costs and data lock-in kept customers in place for decades. Fintech companies can now plug into bank data to offer better budgeting tools, faster loan approvals, and cheaper payments, intensifying competition for every profitable slice of the banking relationship.

The same data-openness battle is playing out in crypto, where exchanges and custodians are positioning for institutional flows. The winners of the open banking era are still being decided, and that uncertainty is precisely where attentive investors find opportunity.

Reading the Regulatory Tea Leaves

Banking regulation moves slowly, which is exactly why it rewards investors who pay attention early. A capital rule proposed today reshapes bank earnings two years from now. A digital asset framework finalized this year determines which platforms and tokens thrive over the next decade. An open banking mandate quietly redraws the competitive map while most of the market watches quarterly earnings instead.

None of this requires a law degree. It requires knowing the three battlegrounds, digital assets, capital requirements, and data openness, and checking in on them a few times a year. Regulation is the rulebook for financial markets, and investors who read it consistently outplay those who only watch the score.